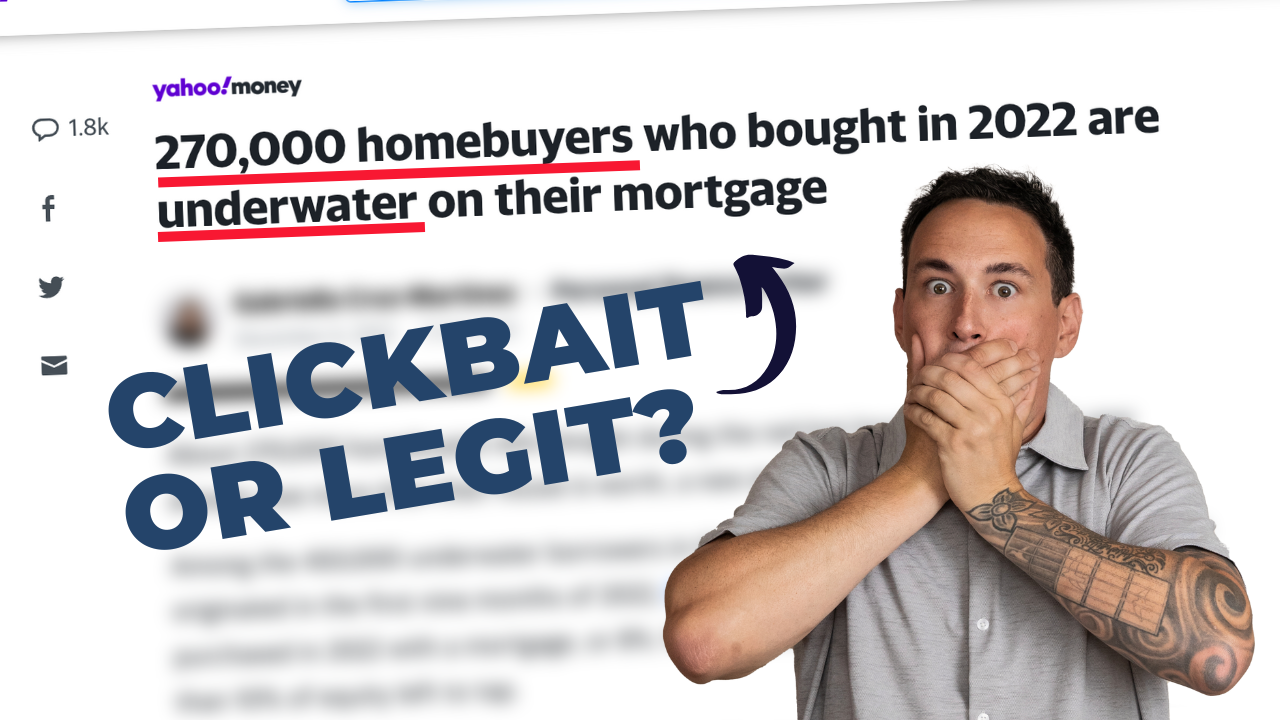

Headlines can be deceiving

A recent article making the rounds claimed that “270,000 homebuyers in the past year are “underwater” on their homes.” Seeing headlines like this can be alarming and potentially misleading, so we decided to break down the claims in this article to evaluate its credibility.

Reading the headline, you might think that buyers have defaulted on their mortgage and aren’t making payments, or perhaps that they owe more than the house is worth.

However, this article defined being “underwater” on a home as having less than 10% equity in their recently-purchased home within the first nine months of 2022. Furthermore, this article was focused exclusively on buyers who used FHA or VA mortgages to purchase homes.

To put that into perspective, FHA homebuyers can put down as little as 3% and VA buyers can put down as little as 0%, making it a completely expected outcome that their equity in their home would be low, especially in a market where houses are selling at list price.

It’s a very different market now

The market shift – from a market where we routinely saw homes go for $50,000 – $100,000 over list price to a market where homes are selling at list price – means slower appreciation. The appreciation we saw during that peak pandemic market of 2020 was anomalous and unsustainable. During the peak seller’s market during the pandemic, prices rose so quickly that people who bought in 2020 had a significant rise in equity in a short amount of time. However, unless you’re making significant improvements and updates, real estate is a long term investment. No matter what market you’re buying in, it’s not common to have positive equity immediately after purchasing.

Another claim this article made is that early payment defaults are up 150%. While that number checks out, what does it mean and is it an indicator of some serious housing crisis on the horizon?

What is Early Payment Default?

Early payment default is defined as two months of missed payments within the first six months of purchasing the home. However, this article is comparing payment defaults in 2022 with numbers from 2013 – 2018. As we all can remember, 2013 – 2018 – pre-pandemic – was a very different market and economy than where we are now. While that doesn’t mean that the rise in payment defaults isn’t concerning, it does suggest that this article is more interested in raising alarm than in presenting data in a principled manner.

Being “underwater” on your mortgage the way the article defines it – having a couple of missed payments – is a non-issue if you can still afford your home in the longer term. However, one topic this article doesn’t address that we feel is something to keep an eye on as an indicator for potential concern is the unemployment rate. While employment is currently quite low, many economists have warned that layoffs are coming. It would be concerning if employment rose and recent homeowners, particularly those with little home equity, couldn’t afford their monthly mortgage payment.

Bottom Line

The bottom line here is that there is a lot of scary-sounding news regarding the housing market including this one. However, it’s important to maintain a level head and talk to someone who can provide context for the claims in an article, no matter how convincing the statistics sound. Reach out to us for practical and considered dialogue on all topics real estate!